Institutional Insights: UBS 'CTAs' Positioning and Flows - Biweekly Update 23/6/26'

The systematic backdrop remains broadly supportive for risky assets and carry, with the key assumption being that realized volatility continues to drift lower. If realized equity volatility declines by around 3 percentage points over the coming weeks, that should mechanically support higher equity exposure from vol-sensitive strategies and allow CTAs to re-leverage into existing uptrends. This reinforces the near-term risk-on setup, particularly in equities, credit, and USD carry. But it is a low-vol regime that remains vulnerable to shocks: CTAs can add in calm markets, but they are still more sensitive to downside moves than upside moves, especially after the recent build in leverage.

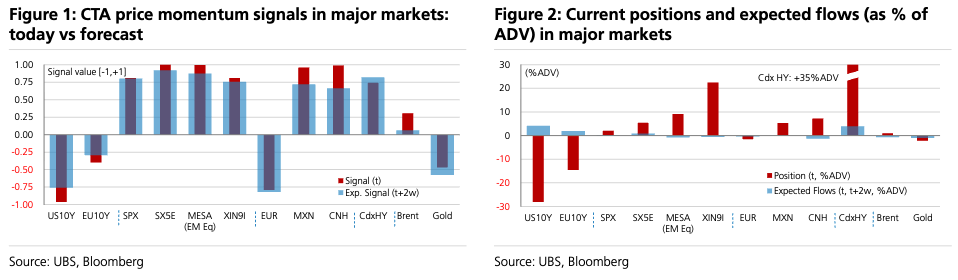

In equities, the CTA signal is bullish across most major markets, with the main exceptions being NIFTY, HSI, HSCEI, and IBOV. That fits the recent tape: US and developed-market equities remain supported by AI, earnings revisions, and liquidity/flow dynamics, while China-linked indices remain weak and India/LatAm are more mixed. A decline in realized volatility should help systematic strategies add exposure, but the caveat is important: downside sensitivity remains higher. If the market absorbs Warsh’s hawkish Fed and the Iran deal holds, CTAs can provide incremental demand. If US-Iran negotiations suffer a setback or rates reprice more hawkishly again, the same strategies can become sellers quickly.

The equity setup therefore remains constructive but more fragile than a simple bullish signal implies. CTAs, vol-control, and other systematic flows can support the market as long as realized vol compresses. But the market is also operating with reduced corporate buyback support due to blackout windows, elevated hedge fund leverage, and more crowded positioning in parts of AI and large-cap Tech. That means systematic re-leveraging can lift the tape, but it can also increase sensitivity to reversal if the macro environment deteriorates.

In bonds, CTAs are still broadly bearish across the board, especially in the front end, but there are signs they have begun to cover duration shorts and remain biased toward further buying. This is especially evident in the US and Japan, with a stronger skew toward the long end of the US curve. That is a meaningful nuance. The headline signal is still bearish bonds, but the marginal flow may be less negative and potentially supportive for long-end duration if yields stabilize or fall. This matters for equities because long-end buying would help financial conditions, duration-sensitive assets, and growth multiples.

The front-end bearish signal is consistent with the post-Warsh repricing. The Fed’s reduced forward guidance and renewed price-stability emphasis leave front-end rates vulnerable to hawkish data interpretation. But the long end may behave differently if lower oil, geopolitical de-escalation, and potential growth concerns support duration demand. A curve that remains flat or flattens further would be consistent with a hawkish Fed but contained long-term inflation expectations. That mix is not ideal for banks, but it can still support long-duration equity assets if the long end does not break higher.

Credit remains one of the cleanest systematic supports. CTAs are long and adding, and the low-volatility summer environment is typically favorable for carry. Events like the World Cup can further suppress realized volatility and encourage carry-seeking behavior. In that context, credit should remain well supported, particularly if equities hold, oil stays lower, and default concerns remain contained. Credit is likely to be at the forefront of the carry trade because it benefits directly from low realized volatility and spread compression.

The risk in credit is that positioning and carry trades can become self-reinforcing until they are not. If volatility stays low, credit spreads can grind tighter and systematic flows can keep adding. But if there is a geopolitical reversal, a hawkish rates shock, or an equity drawdown that challenges the AI leadership complex, credit could be vulnerable because investors may have added exposure under the assumption of suppressed volatility. For now, though, the credit signal is clearly supportive.

FX is the most directional part of the CTA story. CTAs are actively accumulating USD, having bought around $100bn since the last update, with an additional $40-50bn expected over the next two weeks, mainly against G10 FX. This is a major flow. It aligns with Warsh’s hawkish Fed debut, stronger US front-end pricing, and the market’s preference for USD in a world where US nominal yields remain attractive and global growth is uneven. The dollar-long CTA impulse can remain a powerful headwind for EUR, JPY, GBP, and broader G10 FX.

GBP, CNH, and commodity-linked currencies appear most at risk. GBP is vulnerable if UK data weaken or if relative policy expectations shift against the Bank of England. Commodity currencies are exposed to the aggressive CTA selling in commodities, especially energy. CNH is more complicated because the stated current signal is bullish CNH, but China-linked assets remain weak and Asia FX more broadly is bearish. The practical takeaway is that USD strength remains the dominant FX trend, and weaker global commodity momentum plus China equity weakness keeps pressure on several non-US currencies.

The current FX signal is bullish USD, LatAm FX, EMEA FX, and CNH, but bearish G10 FX and Asia FX. That implies the carry trade is not simply “long USD against everything.” It is more nuanced: high-carry or idiosyncratic EM FX can still attract demand, while low-yielding or growth-sensitive G10 and Asia FX remain vulnerable. This is consistent with a low-volatility carry environment in which investors favor positive carry and penalize currencies tied to weak growth, low yields, or commodity softness.

Commodities are the weakest systematic area. CTAs are selling aggressively across all four cohorts, and while the pace may moderate, selling is likely to persist. Energy contracts are the most vulnerable. That fits the broader macro backdrop after the Iran MOU and the sharp unwind of geopolitical risk premium in crude. Managed money had already sold heavily, and CTA pressure adds another mechanical headwind. Lower energy remains helpful for inflation and equities, but the positioning risk is becoming more asymmetric if shorts are extended.

The current commodity signal is bullish but selling in Industrials and Energy, while bearish Precious and Agriculturals. That means the existing trend or signal may not yet be fully negative in some cyclical commodities, but the marginal flow is selling. For energy, this is especially important because a market can remain technically bullish on longer lookbacks while shorter-term CTA models reduce exposure aggressively after a sharp decline. If crude continues lower, more selling can follow; if crude reverses sharply on a geopolitical implementation setback, positioning could fuel a short-covering rally.

The combined cross-asset message is bullish equities, bullish credit, bullish USD, bearish bonds at the headline level, and bearish commodities on flow. That mix is supportive for risky assets as long as lower commodities reduce inflation pressure and USD strength does not become destabilizing. It is not a classic reflationary risk-on regime; it is more of a low-vol carry regime supported by AI momentum, credit stability, and falling oil. In that environment, equities can grind higher, credit can tighten, and USD can remain firm.

The main vulnerability is that the regime depends on realized volatility staying low. If volatility declines as expected, systematic strategies can add risk and carry can perform. If volatility rises due to Fed uncertainty, a bad inflation print, an NFP shock, US-Iran implementation problems, or an AI leadership wobble, the same positioning can amplify downside. CTAs are likely more sensitive to downside equity moves because exposure has already increased, while corporate buyback blackout reduces a key stabilizer.

For equities specifically, this framework argues for staying constructive but respecting event risk. A low-volatility grind can support CTAs, vol-control, and carry flows, helping the market absorb hawkish Fed signals and megacap rotation. But any shock that lifts realized vol can quickly reverse that support. The best setup remains selective: own the secular AI and broadening beneficiaries, but avoid complacency in crowded trades where leverage and volatility have already risen..

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!