Will US CPI Fuel Dollar Fireworks Today?

US Inflation On Watch

Traders are braced for plenty of cross-market volatility today with the latest US inflation readings due this afternoon. Following on from the heavy weakness in recent US labour market data we’ve seen a sharp, dovish shift in the market’s Fed pricing with traders now pricing in a .25% cut next month, followed by at least one further cut ahead of year end. Against this backdrop, today’s data has the potential to either further strengthen this view, leading USD lower, or dilute this outlook, causing a squeeze higher in the Dollar.

Today’s Data Forecasts

On the numbers front, the market is looking for annualised headline CPI to rise to 2.8% from 2.7%. On the monthly readings, core is expected to tick up to 0.3% from 0.2% prior with headline seen cooling to 0.2% from 0.3%. If we see a mild uptick in inflation, in line with forecasts, this shouldn’t alter the view on September rates too much, keeping USD skewed lower, though might cause some uncertainty beyond September. If we see an upside surprise today, closer to 3%, this could cast more doubt over the near-term rates outlook, leading USD higher in the short-term. Finally, a downside surprise today would be seen as cementing the dovish Fed outlook, fuelling a firmer sell-off in USD. With equities and the broader risk complex set to take their cue from today’s data, this release could be pivotal for markets ahead of that September FOMC meeting.

Technical Views

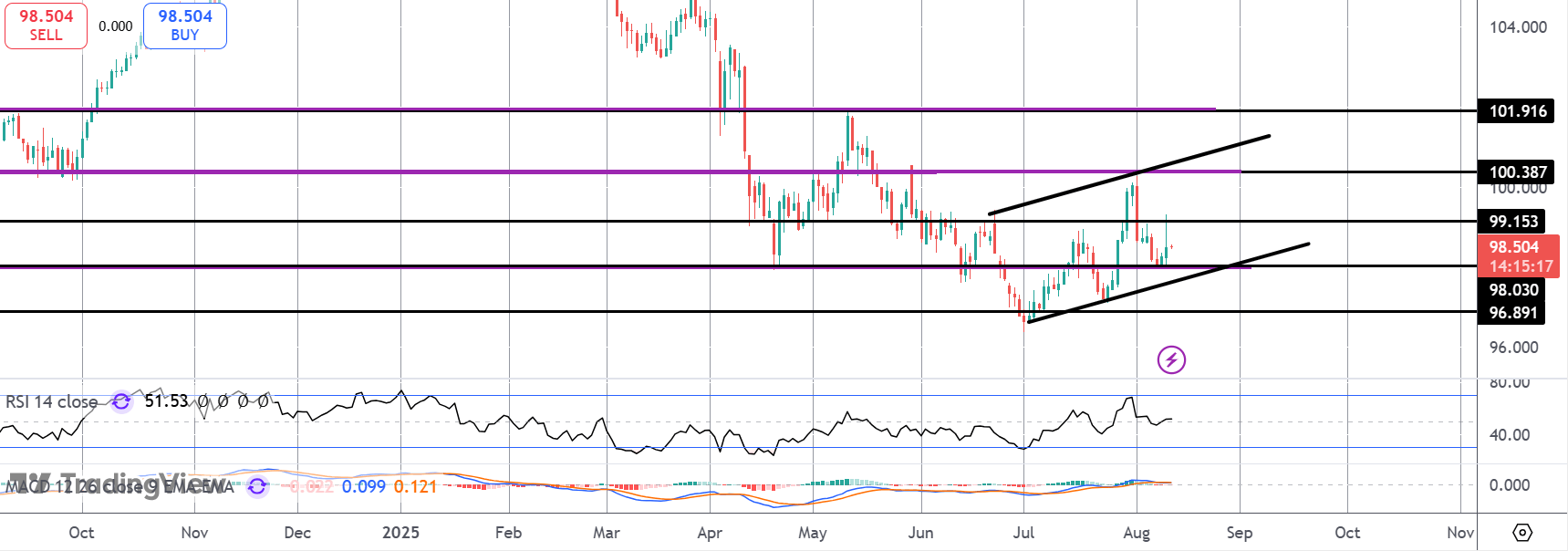

DXY

For now, the index remains within the bull channel off YTD lows. While 98 holds as support, price could see a fresh test of the 99.15 resistance with the 100.38 level sitting above as the higher bull target. Should we break current support, however, focus shifts to 96.89 as the next support to watch around the YTD lows.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

With 10 years of experience as a private trader and professional market analyst under his belt, James has carved out an impressive industry reputation. Able to both dissect and explain the key fundamental developments in the market, he communicates their importance and relevance in a succinct and straight forward manner.