Institutional Insights: Credit Agricole FX Weekly 1/5/26

The ongoing conflict between the US and Iran has reignited the "risk-on, risk-off" (RORO) dynamic in the foreign exchange market. In March, escalating tensions from the Iran war dampened market enthusiasm, leading to a surge in demand for the safe-haven US dollar. However, as a ceasefire brought some relief in April, investor confidence rebounded, causing the dollar to lose ground. This RORO theme is closely linked to concerns that the conflict could disrupt energy supplies, negatively impacting economies reliant on energy imports while benefiting those that export energy.

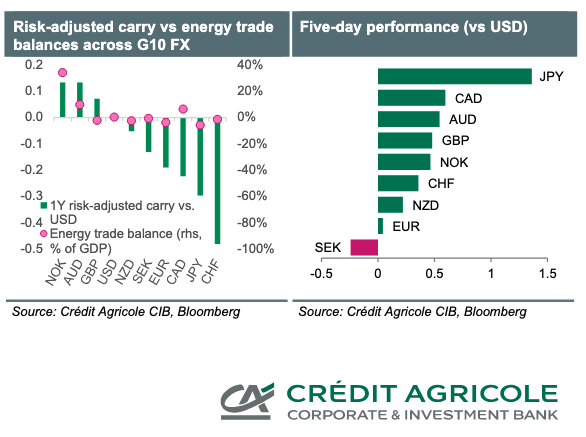

As a result, high-yielding G10 currencies from energy-exporting nations like Australia (AUD) and Norway (NOK), alongside the USD, have gained traction. This trend was further fueled in April by increased interest in FX carry trades, which are funded by low-yielding currencies from energy-importing countries such as Japan (JPY) and Switzerland (CHF).

Interestingly, some investors have pointed out that improved risk appetite isn't the only reason the dollar has struggled to maintain its initial gains. They attribute this underperformance to concerns over the potential repercussions of US attempts to "weaponize" the dollar. While the Iran conflict may bolster the long-term trend towards de-dollarization, our analysis hasn't shown any significant resurgence in the "Sell America" narrative; in fact, foreign demand for US stocks rebounded in April. However, elevated costs for USD FX hedging have meant that many of these investments remained unhedged.

Looking ahead, market attention will likely remain fixated on US-Iran tensions and their influence on global energy prices and overall risk sentiment. In addition to geopolitical factors, investors will be keenly observing upcoming US economic data—such as Non-farm payrolls and services ISM—as well as comments from Federal Reserve officials.

Meanwhile, the Japanese yen (JPY) experienced a notable surge following Japan's first official FX intervention since 2024. The Ministry of Finance may continue to monitor the situation closely, especially during the lower liquidity period of the Golden Week holiday, potentially intervening again to bolster the yen.

In other developments, we anticipate that demand for FX carry trades will remain a significant market driver, positively impacting currencies like AUD and NOK. We expect the Reserve Bank of Australia (RBA) to announce a rate hike next week, although it may come with a split decision and dovish language that could weigh on the AUD. The Norges Bank is also at a crossroads; after signaling a return to rate hikes during its March meeting, it faces a tight decision on whether to act next week. The tightening effect of strong NOK gains since then might afford the bank a bit more time before making any moves.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!