S&P500 Daily Action Areas & Price Targets 3/7/26

S&P500 Daily Action Areas & Price Targets 3/7/26

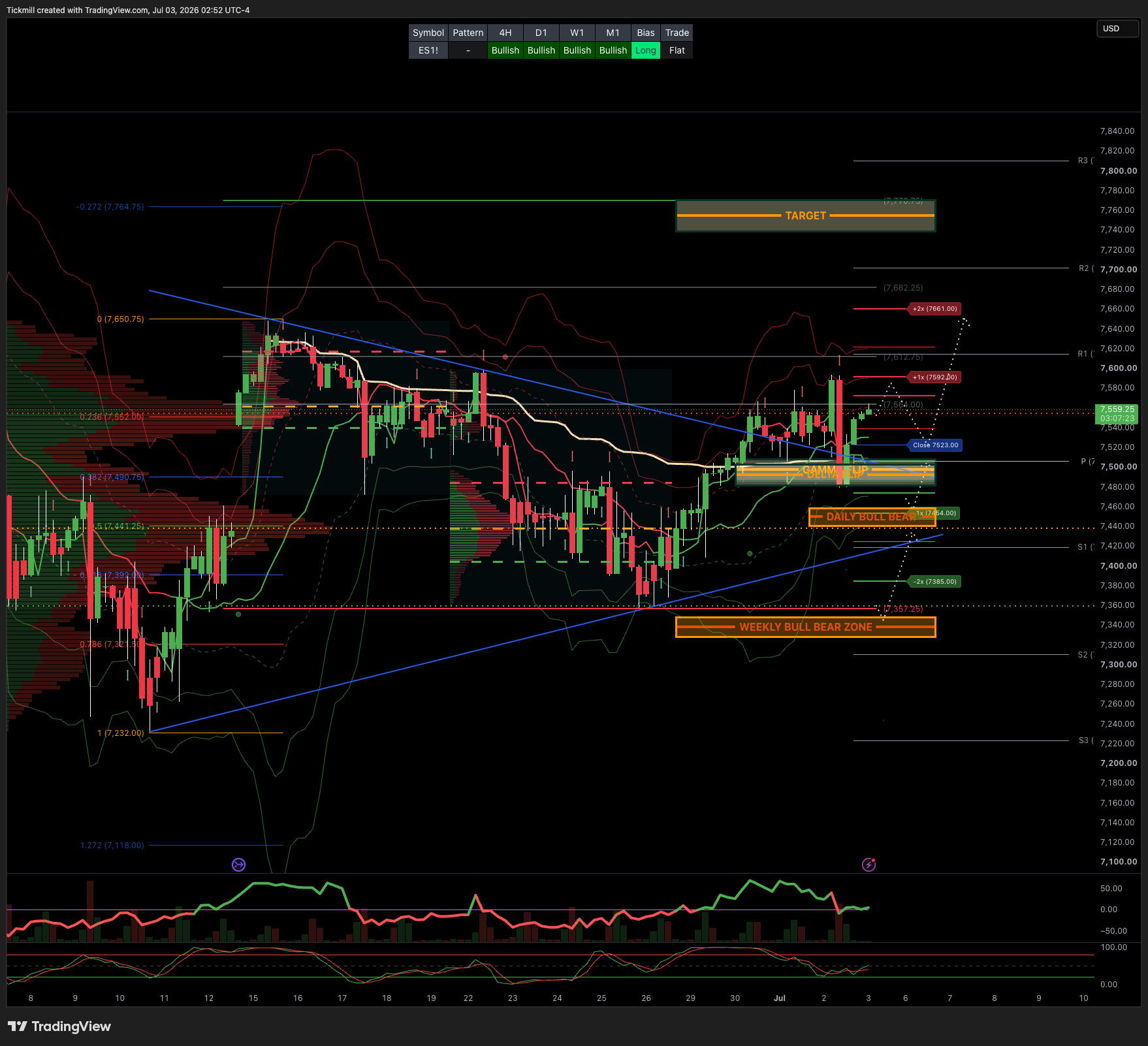

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7350/40

WEEKLY RANGE RES 7280 SUP 7520

MONTHLY RANGE RES 7932 SUP 7384

JHEQX Q3 Collar Short Call Cap: ~7,750 – 7,900 - Long Put Strike: ~7,050 – 7,100 (approx. 5% downside protection) Short Put Strike: ~5,950

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.07 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish.

GS Flow Desk: large S&P 31Aug 7000/7950 strangle in roughly $20mm vega / $115mm premium

My Read – classic “big convexity versus carry” trade: either someone paid a lot to own a wide August move, or someone got paid a lot to bet that the S&P stays comfortably inside the 7000–7950 corridor

DAILY VWAP BULLISH 7440

WEEKLY VWAP BULLISH 7494

MONTHLY VWAP BULLISH 7036

DAILY STRUCTURE - OTFH 7495

WEEKLY STRUCTURE - BALANCE 7648/7247

MONTHLY STRUCTURE - OTFH - 7199

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFL): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7450/7450

GAMMA FLIP 7497

DELTA FLIP 7493

DAILY RANGE RES 7592 SUP 7454

2 SIGMA RES 7661 SUP 7385

VIX BULL BEAR ZONE 17.4

TRADES & TARGETS

LONG ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET DAILY RANGE RES ***ACTIVE FROM 2/7/26 PLAN**

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS FICC & EQUITIES TRADING DESK VIEWS

Market Takeaway — Momentum Shock, Softer Labor, Lower Hike Risk

“He who is brave is free” is a fitting line for this tape: the market is forcing investors to decide whether to hold the broader bullish equity view while stepping away from the most crowded expressions of it.

Stocks traded lower into the long weekend on muted activity, but the real story again was factor violence, not broad index collapse. The High Beta Momentum pair trade fell another 8.6%, extending the two-day drawdown to roughly 18%, the worst two-day selloff since Covid. That is a remarkable move, but it comes after an extraordinary +57% return in 1H26, so the key question is whether this is a true regime change or a start-of-quarter asset reallocation after an extreme run.

For now, the answer looks closer to violent reallocation than full regime change, but the burden of proof has shifted. Momentum was crowded, had rising realized volatility, and was entering a tough summer seasonal window just as the market was beginning to broaden. That is a dangerous combination. Since Covid, the average momentum peak-to-trough drawdown has been around 12% over 24 days. The current drawdown is already roughly 24% over only 10 days, so the speed and scale are exceptional. Even if the long-term AI/quality infrastructure theme remains intact, factor positioning is clearly being reset.

The macro catalyst was the softer NFP print. Payrolls rose only 57k, well below consensus of 113k, with a -74k downward revision to April and May. The unemployment rate printed 4.19%, below consensus of 4.3%, but that was driven by a decline in participation rather than obvious labor-market strength. Average hourly earnings were in line at 35bps. The sector detail was mixed: employment continued to rise in professional and business services, social assistance, and health care, while leisure and hospitality fell 61k, reflecting weaker-than-usual seasonal hiring.

The labor report is soft enough to reduce hike risk, but not necessarily weak enough to trigger an immediate growth scare. That nuance matters. After Warsh’s first FOMC meeting on June 17 came in more hawkish than expected, the market had been consistently pricing roughly 40bps of hikes by year-end. After the payrolls miss, that dropped to around 28bps, and the expectation is that it likely trends lower through the session and into next week. In the immediate term, that should be supportive for equities because it removes some of the rates pressure that had been building under the surface.

This creates an unusual mix: macro relief, factor stress. Softer payrolls should help duration assets, software, housing, small caps, and some rate-sensitive cyclicals, especially if the market shifts from “Warsh will hike” toward “the Fed can stay patient.” But that same environment may continue to hurt crowded momentum books if investors use lower yields to rotate into laggards rather than chase the first-half winners. Lower hike odds can support the index while still accelerating the broadening trade.

The GS Prime Brokerage data reinforces that interpretation. Global Fundamental L/S managers had an exceptional quarter, finishing Q2 up 18.4%, their strongest quarterly return in the dataset going back to 2016. But rather than press winners, managers cut risk aggressively. US Fundamental L/S gross leverage fell 11.3 points MoM to 199.8%, a one-year low, while net leverage fell 4.2 points to 50.8%, just the 4th percentile over one year. This is not forced de-risking from poor performance; it is profit protection after a record quarter.

The sector rotation is even more revealing. Information Technology saw the largest net selling on record, driven primarily by short sales and, to a lesser extent, long sales at a 2-to-1 ratio. The most net sold subsectors were Semis & Semi Equipment, Tech Hardware, and Communications Equipment, while Software was the most net bought. That is a major shift. The market is rotating out of AI bottleneck / hardware / supplier winners and back toward software, hyperscaler-adjacent names, and rate-sensitive growth laggards.

At the same time, non-consumer cyclicals were net bought for the first time in five months, as buying in Financials, Real Estate, and Energy outweighed selling in Industrials and Materials. This supports the broader “broadening” thesis. The market is not simply selling risk; it is reallocating risk. The beneficiaries are laggards, cyclicals, rate-sensitive groups, and software. The funding source is crowded AI infrastructure and high-beta momentum.

The key point is that this can be constructive for the S&P even if it is painful for many portfolios. If the market broadens into software, financials, real estate, housing, healthcare, and select cyclicals, index performance can remain resilient. But if managers are long the same AI infrastructure winners and short the same laggards, they can experience severe drawdowns despite a relatively benign index tape. That is exactly what has been happening.

The debate now is whether momentum’s selloff becomes self-reinforcing. A two-day 18% decline is large enough to trigger risk limits, VaR reductions, and further unwinds from systematic and fundamental managers. The fact that the current episode is already larger than the average post-Covid drawdown suggests some capitulation has occurred, but the shorter duration also suggests the process may not yet be complete. Summer liquidity, buyback blackouts, and holiday-thinned markets can amplify these moves.

Still, the macro setup after NFP is not hostile. Lower hike pricing, softer labor data, contained wage pressure, and likely lower yields should help equities into earnings, especially if investors interpret the report as a slowdown toward trend rather than a break in the labor market. The risk would be if subsequent data confirm a sharper deterioration in hiring, particularly outside leisure and hospitality, or if lower participation begins to undermine the benign interpretation of the unemployment rate.

For the immediate tape, the practical read is:

- Bullish for index duration / rate-sensitive areas: lower hike odds help software, housing, real estate, and parts of small caps.

- Bearish for crowded momentum: the factor unwind may continue as investors rotate away from first-half winners.

- Constructive for broadening: financials, real estate, software, healthcare, and lagging cyclicals should remain in focus.

- Mixed for AI infrastructure: secular fundamentals remain strong, but positioning and first-half performance are major headwinds.

- Supportive for earnings setup: unless the labor data deteriorate further, lower rate pressure into Q2 earnings is helpful.

The “regime change” question depends on whether the AI infrastructure earnings story breaks. So far, there is no decisive evidence of that. What has changed is the market’s willingness to pay any price for the most crowded beneficiaries. That argues for a factor regime shift, not necessarily an equity bull-market regime shift. Momentum leadership may be challenged, but equities can still trend higher if earnings broaden and rate pressure eases.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!