S&P500 LDN Open Trading Update 18/5/26

S&P500 LDN Open Trading Update 18/5/26

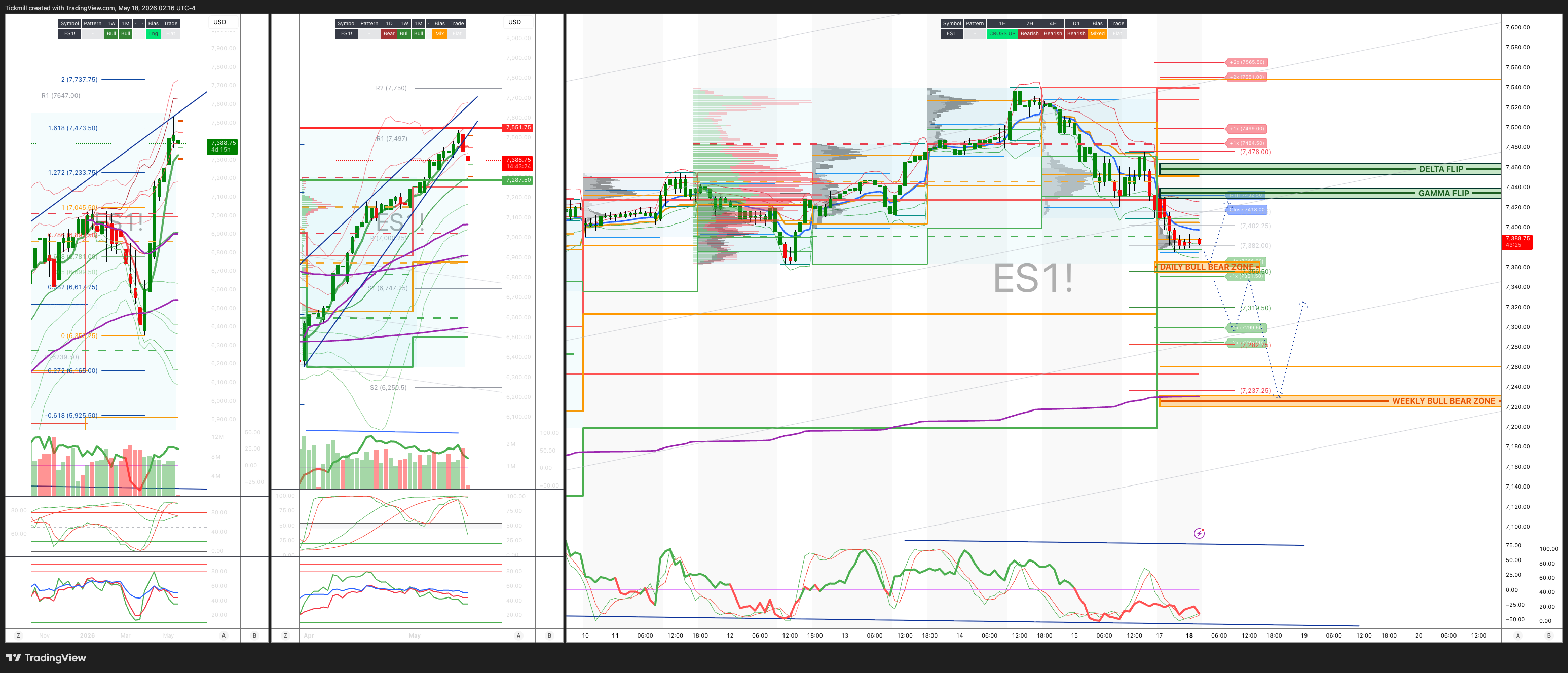

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7220/30

WEEKLY RANGE RES 7286 SUP 7550

June MOPEX Straddle: 274pt range implies a OPEX to OPEX range of [7134, 7683]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 0.96 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BEARISH 7455

WEEKLY VWAP BULLISH 7292

MONTHLY VWAP BULLISH 6898

DAILY STRUCTURE – BALANCE - 7540/7399

WEEKLY STRUCTURE – OTFH - 7363

MONTHLY STRUCTURE - OTFH - 6514

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Down (OTFD): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7350/60

GAMMA FLIP 7434

DELTA FLIP 7455

DAILY RANGE RES 7499 SUP 7351

2 SIGMA RES 77551 SUP 7299

VIX BULL BEAR ZONE 19.47

TRADES & TARGETS

LONG ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET RTH/CLOSE

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Weekly Mash’

Amazon, AI, and the Market’s Capacity for “Useful Excess”

Amazon IPO’d 29 years ago at USD 18/share, equivalent to USD 0.075/share adjusted for its four stock splits. From that split-adjusted IPO price to last night’s close, the stock has returned roughly 3,563x. The IPO itself raised just USD 54mn from a 3mn share offering.

That historical reference is useful because it captures the uncomfortable truth about equity markets: they are not designed to allocate capital perfectly in real time. They are reactive, forward-looking, and prone to excess. But those excesses are also part of how the market funds the next generation of compounders.

The central point: today’s apparent misallocation of capital can become tomorrow’s innovation cycle. A lot of capital will be wasted, but a small number of Amazons, Nvidias, or future AI winners can pay for many Pets.coms.

The market may be stretched, but not necessarily irrational

There has been understandable pushback against the idea that the market is not yet truly irrational. Semis, AI, space stocks, and high-beta innovation names have had eye-watering moves. Yields are breaking higher. Inflation risks are rising. Breadth has been narrow.

But the counterargument is that markets often look irrational during periods when the long-term opportunity set is genuinely expanding. That was true in the late 1990s, even though the bubble eventually burst. Many companies failed, but the capital cycle funded infrastructure, experimentation, and business models that created enormous long-run value.

The same argument applies today. AI-led innovation is opening new upside optionality, and unlike many prior speculative cycles, today’s investment is being funded heavily by mega-cap tech companies with massive free cash flow. That makes the cycle more durable than a purely debt- or retail-funded bubble.

Creative destruction requires excess

The Amazon example is not meant to say every AI or space stock is the next Amazon. Most will not be. The point is that capitalism’s innovation engine often requires overfunding.

Excess capital creates:

Failed experiments

Overcapacity

Fraud and hype

Valuation mistakes

But also breakthrough infrastructure

New platforms

New industries

Future dominant firms

The market’s “bug” is also its feature. It repeatedly overfunds promising frontiers, destroys weak companies, and leaves behind a few extraordinary winners.

That is why the right question is not simply, “Is there excess?” There clearly is. The better question is: is the excess funding a real technological frontier with durable productivity potential? On AI, the answer increasingly looks like yes.

AI capex is still the core bullish anchor

The AI cycle remains supported by record capex from the largest and most profitable companies in the market. This distinguishes the current cycle from more fragile speculative episodes.

The behemoth tech companies are internally funding enormous investments in:

Data centers

Semiconductors

Networking

Memory

Power

Cooling

Software infrastructure

AI model deployment

This matters because the investment cycle is not dependent solely on cheap external financing. It is being driven by companies with fortress balance sheets, high margins, and strategic urgency.

That does not eliminate valuation risk, but it supports the idea that the AI infrastructure cycle can run longer than many expect.

High-beta momentum is flashing caution

That said, some objective warning signs are building.

Monday saw the high-beta momentum pair post its largest up day on record. Meanwhile, the desk’s Risk Appetite Indicator and Equity Momentum pair reached concurrent highs of this kind for the first time since 2000.

Those are not trivial signals. They do not prove an immediate top, but they indicate that investors are aggressively chasing upside. When risk appetite and momentum both hit extremes, future returns become more dependent on continued inflows and favorable macro conditions.

So the message is balanced:

Broad tech and AI can remain fundamentally attractive.

But some parts of the market are entering momentum-excess territory.

This is a time to be constructive, not complacent.

Memory is becoming the new inflation problem

The market initially worried about shortages of energy and jet fuel. But in AI, the more acute bottleneck may be memory.

Memory shortages and tech component inflation are becoming macro-relevant because AI capex is so large that it is affecting broader supply chains. This inflation risk is no longer only about oil. It is also about chips, memory, power equipment, and data-center components.

That is feeding into long-end yield pressure globally. The inflation fear is now twofold:

Energy shock from the Strait/Middle East.

AI supply-chain/component inflation.

This is one reason long-end yields have become the market’s main vulnerability.

Taiwan overtakes China in EM index weight

One striking consequence of the AI cycle is that Taiwan has overtaken China in MSCI EM index weight, with TSMC representing roughly 57% of Taiwan’s weight.

This is a major structural shift. EM exposure is becoming less about broad China growth and more about AI hardware supply chains. Index composition is being reshaped by semiconductors.

The implication is that global investors who own EM benchmarks are increasingly long the AI supply chain whether they intend to be or not.

Bonds are the main constraint

The biggest risk to the equity rally is not that AI is fake. It is that bond yields rise enough to challenge valuations.

US 10-year yields are threatening to break out. Long-end yields globally are moving to uncomfortable levels as markets price:

Energy-driven inflation

AI component inflation

Large fiscal deficits

Defence spending

Energy security spending

Less confidence in central-bank easing

Question marks over Fed independence

This is why equities have been spooked late in the week. The AI story can justify higher earnings and long-term productivity gains, but if discount rates keep rising, multiples become harder to sustain.

UK: gilts hit pre-Amazon-era yield levels

The UK is facing its own version of the bond problem, amplified by politics. Labour is turning on Starmer, and markets may now face weeks of uncertainty around Andy Burnham potentially winning a by-election and then a months-long Labour leadership process.

UK 10-year yields are now at levels not seen since before Amazon’s IPO and above the levels reached during the Liz Truss crisis.

The UK issue is not just inflation. It is also:

Political instability

Fiscal credibility

Weak structural growth

Reduced LDI demand

Sterling’s lack of reserve-currency status

Scarring from prior fiscal shocks

This keeps UK term premium structurally elevated and makes it hard to fade the gilt selloff without political clarity.

Fiscal spending remains a growth support, but also a rates risk

The global economy is being supported by a strange mix of unaffordable fiscal spending and private-sector capex.

In the US, the primary deficit remains close to 7%, which is a significant support to demand. In Germany, the defence spending trajectory may rival even bullish AI capex projections.

This helps growth and corporate revenues in the near term. But it also creates a bond-market problem because large deficits and investment needs require financing at a time when inflation is elevated and central banks are less able to cut.

So fiscal spending is both:

A growth tailwind for equities

A term-premium headwind for bonds

Narrowness is starving other good opportunities

Even with a constructive view on broad tech, the narrowness of the market is creating distortions. Capital is being sucked into AI and mega-cap tech, leaving other credible opportunities neglected.

Examples include:

European aerospace

European defence

Select industrial beneficiaries

Companies with strong earnings but weak price action

The Rheinmetall example is telling: earnings have improved, but the stock has been stuck in an out-of-fashion neighborhood. That suggests the market’s narrow focus may be creating relative-value opportunities outside AI.

AI productivity is the key macro variable

Jan Hatzius’s “Bending, Not Breaking” framework is critical. The market is facing a long list of negative macro topics:

Oil supply shock

Large fiscal deficits

Fed independence concerns

Population shrinkage

Cyber and AI security risks

US-China rivalry

War in Europe

High valuations

And yet equities have performed well. The likely explanation is strong earnings plus a better long-term productivity outlook from AI.

US productivity has already accelerated from a pre-pandemic trend of about 1.5% to 2.1% since the pandemic. The argument is that the improvement can continue as AI adoption broadens.

This matters enormously for equities because long-dated earnings and dividends represent a large share of fundamental value. Goldman strategists estimate that for the US market, earnings and dividends a decade or more in the future represent roughly 75% of fundamental value.

If AI raises the long-term productivity and profit path, it can justify a higher equity market even amid near-term macro stress.

The core tension: productivity boom versus bond shock

The market is effectively balancing two forces.

Bullish force: AI productivity and earnings

Strong Q1 earnings

Mega-cap funded AI capex

Long-term productivity upside

New business models

Infrastructure buildout

Software adoption

Potential margin expansion over time

Bearish force: inflation and yields

Energy shock

Memory/component inflation

Long-end yield breakout risk

Fiscal deficits

Political instability

Central-bank credibility questions

Narrow leadership

This is why the market can be both fundamentally exciting and tactically dangerous.

Trading implications

The right stance is not to dismiss the AI move as simply irrational. The innovation cycle is real, and the Amazon analogy reminds us that huge long-term winners often emerge from periods that look excessive at the time.

But the risk-management message is equally important:

Stay constructive on broad AI infrastructure and software.

Avoid indiscriminately chasing the most parabolic semi or high-beta momentum names.

Watch memory prices and component inflation as macro variables.

Treat long-end yields as the key constraint on equity multiples.

Look for neglected opportunities in European aerospace, defence, and industrials.

Be careful with UK duration until political and fiscal uncertainty clears.

Use pullbacks in quality AI names rather than chasing euphoric upside days.

Consider that the best future compounders may not be the most obvious current winners.

The Amazon IPO anniversary is a reminder that equity-market excess is not always useless. Markets overfund frontiers, destroy capital in weak companies, and occasionally create world-changing compounders. AI may be another version of that cycle.

The current market does show signs of excess: high-beta momentum records, extreme AI/semi performance, narrow leadership, and pressure on bond yields. But it is not irrational to believe that AI can raise productivity and long-term profits, especially when the capex cycle is funded by the strongest companies in the world.

The practical conclusion is: respect the innovation cycle, but manage the bond-market risk. Stay constructive on AI, but be selective, avoid chasing the most extended names, and treat rising long-end yields as the main threat to the rally.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!