Institutional Insights: Goldman Sachs US Weekly Kickstart 18/5/26

US Weekly Kickstart: EPS Revisions Still Matter, but AI Momentum Is Running Ahead of Analysts

The market remains narrow and momentum-heavy, but beneath the surface stocks are still broadly trading in line with earnings revision trends. Goldman’s sector-neutral long/short EPS revision factor — long S&P 500 stocks with the strongest recent 2-year forward EPS revisions and short those with the weakest — struggled early in the war but has since recovered and is now up 8% YTD.

The key message: earnings revisions are still driving stock selection, but AI semis and momentum winners are increasingly pricing long-term earnings growth beyond what analysts have yet embedded in estimates.

EPS revision factor has recovered

Goldman’s EPS revision factor compares returns of S&P 500 stocks with the strongest versus weakest recent revisions to consensus 2-year forward EPS estimates, while keeping the factor sector-neutral.

The factor initially struggled in the first weeks of the war, when macro shock, energy prices, and positioning overwhelmed fundamentals. But it has since recovered and generated a long/short return of 8% YTD.

That matters because it suggests the market is not purely speculative. Even in a momentum-heavy AI tape, earnings revisions are still being rewarded.

AI infrastructure and Energy are driving S&P 500 EPS upgrades

The majority of upward revisions to S&P 500 EPS estimates have come from AI infrastructure stocks and Energy.

YTD cumulative change in consensus 2027 EPS estimates:

Group | 2027 EPS revision |

|---|---|

AI infrastructure stocks | +32% |

Energy | +19% |

S&P 500 | +8% |

S&P 500 ex-AI infrastructure & Energy | ~0% |

This is one of the most important points in the report. The broad index looks like it is enjoying solid earnings upgrades, but the revision strength is concentrated. Excluding AI infrastructure and Energy, S&P 500 2027 EPS estimates are basically flat YTD.

So the market’s earnings story is real, but it is not broad.

Revision breadth is positive across every sector

Despite concentration at the index level, EPS revision breadth is positive across all S&P 500 sectors. In other words, positive revisions have outnumbered negative revisions in every sector.

The strongest breadth appears in areas like:

Information Technology

Energy

Industrials

Utilities

The weaker but still positive breadth appears in areas like:

Consumer Discretionary

Consumer Staples

Financials

This is constructive because it means analysts are not broadly cutting numbers. However, the magnitude of revisions remains heavily skewed toward AI infrastructure and Energy.

Industry returns mostly align with EPS revisions

Since the start of the war in February, most S&P 500 industry groups with positive 2027 EPS revisions have generated positive returns, while those with negative revisions have generally lagged.

This confirms that earnings revisions are still directionally relevant.

However, there are exceptions:

Materials have traded lower despite upward EPS revisions.

Autos have rallied despite downward revisions to 2027 EPS estimates.

Those exceptions likely reflect positioning, tariff expectations, commodity volatility, policy risk, or investors looking through near-term estimate changes.

Energy: strongest revisions, modest returns

Energy has had the strongest recent upward EPS revisions among industries. Consensus 2027 EPS forecasts have risen +26% since before the war, but the sector has returned only +4%.

That is a major gap. It suggests energy equities are not fully discounting the earnings benefit of higher prices, possibly because investors are skeptical about the durability of oil prices, worried about political intervention, or reluctant to pay higher multiples for commodity-driven earnings.

Potential explanations:

Investors view energy upgrades as cyclical and temporary.

Political risk around windfall taxes or consumer relief is rising.

ESG and mandate constraints limit inflows.

The market prefers AI’s secular growth over energy’s commodity beta.

Higher oil is seen as a macro tax that could eventually hurt demand.

From a relative-value standpoint, Energy looks under-owned versus the scale of EPS revisions.

Semis: prices have outrun revisions

Semiconductors are the opposite case. Semis have outperformed their recent EPS revisions significantly.

This does not necessarily mean the move is wrong. It means equity prices are discounting a future earnings path that analysts have not yet fully incorporated. In other words, the market is moving ahead of estimate revisions.

Potential drivers include:

Leveraged ETF inflows

AI momentum

Long-term data-center demand

Memory shortage pricing power

Structural margin upside

Scarcity value

Index and benchmark pressure

Investor fear of missing the AI trade

The risk is that once prices move far ahead of revisions, the sector becomes more vulnerable to any disappointment in orders, margins, supply chain, or yields.

Market prices are embedding long-term AI upside

Goldman’s interpretation is that when returns diverge from revisions, market prices may be doing one of two things:

Moving ahead of analysts, embedding expectations for long-term earnings growth not yet reflected in consensus.

Pricing a risk distribution that differs from the central earnings estimate, such as upside optionality, scarcity value, or downside hedge demand.

For semis, both are likely true. Analysts may still be too conservative on long-term AI demand, but market prices are also paying aggressively for optionality.

This is why semis can keep working even if near-term EPS revisions do not fully justify the move — but it also raises drawdown risk if momentum reverses.

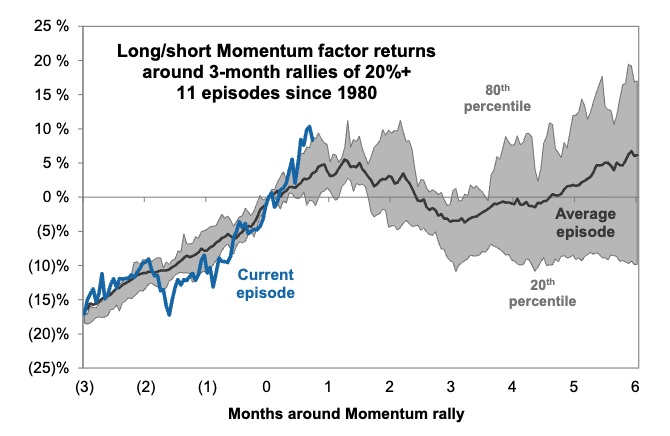

How to hedge AI momentum reversal

Goldman notes that one way to protect against an AI or Momentum reversal is to own some low Momentum stocks.

This is counterintuitive but historically important. In the sharpest Momentum reversals of the past 100 years, previous laggards did not merely outperform on a relative basis — they actually appreciated in absolute terms.

That matters because a momentum unwind is not always just “winners fall.” It can also be a violent rotation into prior laggards.

A practical hedge is to own low-Momentum stocks that also have positive recent EPS revisions. That avoids buying low-quality losers and instead targets laggards where fundamentals are improving.

Low Momentum with positive revisions: why it works

This combination can work because it offers three advantages:

It hedges against a momentum reversal.

It avoids purely distressed or value-trap names.

It provides fundamental support from improving estimates.

In a reversal, crowded winners may be sold to fund purchases of neglected names with improving earnings. That can create positive absolute returns in low-Momentum revision-up stocks.

This is particularly relevant now given the extreme moves in AI, semis, high-beta momentum, and retail-favorite baskets.

“Insensitive Portfolio”: opportunities outside AI and macro beta

For investors looking beyond Momentum and AI, Goldman highlights an Insensitive Portfolio.

The screen selects Russell 1000 stocks with:

Positive recent EPS revisions

Low share-price sensitivity to the AI trade

Low share-price sensitivity to US economic growth pricing

Goldman proxies US economic growth exposure using the relative returns of equal-weight Cyclicals versus Defensive sectors. AI exposure is measured using the GS AI basket pair.

During the past year, these two exposures explained about 30% of daily return variation for the median Russell 1000 stock, but only 13% for the median stock in the Insensitive Portfolio screen.

The idea is to find stocks where returns are less dependent on the two dominant macro factors: AI enthusiasm and US growth expectations.

Why the Insensitive Portfolio matters now

This screen is useful because the market has become heavily organized around two axes:

AI winners versus AI laggards

Cyclicals versus defensives / growth pricing

If a stock has low sensitivity to both and positive EPS revisions, it may offer cleaner alpha. These stocks may be less vulnerable to:

AI momentum reversals

Growth scares

Yield spikes

Crowded factor unwinds

Macro headline volatility

In the current environment, that is valuable diversification.

Trading implications

The most important trading takeaway is that the market is still rewarding EPS revisions, but momentum and AI have created large valuation and return gaps.

AI infrastructure: still has the strongest earnings revision support. Stay constructive, but recognize that some names are now very crowded.

Semis: remain structurally supported, but prices have moved ahead of revisions. Risk/reward is less clean after extreme outperformance.

Energy: looks relatively attractive versus revisions. EPS upgrades are substantial, but stock returns have lagged. Could be a source of catch-up if oil remains high.

Materials: may offer selective opportunities where positive EPS revisions have not been rewarded.

Autos: caution warranted, because price gains have occurred despite downward revisions.

Low Momentum + positive revisions: useful hedge against a Momentum reversal.

Insensitive stocks: useful for investors seeking alpha outside AI and macro-growth beta.

The market is not ignoring fundamentals. EPS revisions continue to matter, and the long/short revision factor is up 8% YTD. But the earnings story is highly concentrated: AI infrastructure and Energy are doing most of the work, while the S&P 500 excluding those groups has seen essentially no 2027 EPS upgrade YTD.

The key divergence is between Energy and Semis. Energy has seen the strongest EPS upgrades but modest returns, while Semis have surged beyond current revisions as investors price long-term AI upside. That does not make semis wrong, but it makes them more vulnerable to a momentum reversal.

The best portfolio response is to stay exposed to AI quality, add selective exposure to revision-supported laggards, and use low-Momentum positive-revision stocks or Insensitive Portfolio names as hedges against an AI/momentum unwind.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!